Through a series of landmark policy decisions, from granting special exemptions for key projects to adjusting system governance indicators, the State Bank of Vietnam is sending a strong signal about a focused credit expansion cycle, ready to inject trillions of dong into the economy

Unprecedented "special treatment"

The most groundbreaking highlight in recent credit management is Document No. 5386/NHNN-TD, issued by the State Bank of Vietnam, which allows the exclusion of outstanding loans for 18 key projects from the credit growth limit (room). This is a special mechanism for three "giants" including Vingroup, Sun Group, and Masterise, with a total capital requirement of up to VND 752,000 billion (approximately USD 28 billion) in the period 2026-2028.

This capital flow is not dispersed but is directly directed towards strategic infrastructure such as: urban railways (Ben Thanh - Can Gio, Hanoi - Quang Ninh), expansion of Phu Quoc International Airport, Gia Binh Airport, and other large infrastructure complexes… The exemption from the foreign ownership limit for these mega-projects allows commercial banks to disburse funds more aggressively without worrying about reaching their annual growth ceiling. However, the regulator maintains strict discipline by requiring separate monitoring of this outstanding debt to ensure that the borrowed capital is used for its intended purpose

Not only focusing on specific projects, the State Bank of Vietnam (SBV) also implemented systemic changes through Circular 25/2026/TT-NHNN. After years of tightening regulations to ensure safety, the SBV officially raised the maximum ratio of short-term capital used for medium and long-term lending from 30% to 40%. This is considered a strategic reversal.

With short-term funding accounting for 80-90% of total system-wide funding, this change helps "free up" an additional 1.3 - 1.5 trillion VND in medium- and long-term lending capacity – a source of capital that is currently in high demand for infrastructure and energy projects.

Circular 25 will take effect from July 1st 2026

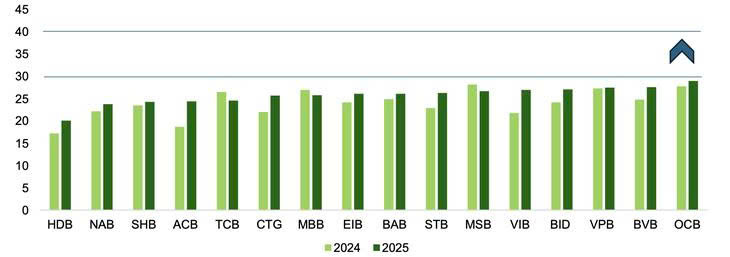

The ratio of short-term capital to medium- and long-term loans of some banks.

Simultaneously, Circular 08/2026/TT-NHNN allows banks to include 20% of State Treasury deposits in their funding sources when calculating the loan-to-deposit ratio (LDR). This is particularly beneficial for state-owned banks (Vietcombank, BIDV, VietinBank), helping them reduce capital costs and creating more room to lower lending interest rates.

Opportunities for the economy and challenges for the banking system.

A series of consecutive moves to loosen risk management controls has sparked mixed opinions regarding the system's safety. Experts warn of liquidity risks due to the "short-term gains for long-term gains" approach and the mismatch in maturities between assets and liabilities.

Overall, the policies issued in the short term all share a common point: expanding the credit growth space for the banking system. Relaxing the loan-to-deposit ratio (LDR) gives banks more room for credit growth without putting excessive pressure on capital costs

Raising the short-term capital ceiling for medium- and long-term loans helps increase the supply of long-term credit; while mechanisms to exclude outstanding debt from credit control limits facilitate a stronger flow of capital into priority sectors and key projects

Financial institutions also have a fairly positive view. Vietcombank Securities (VCBS) assesses this as a calculated easing measure. Banks will have to upgrade their governance capacity (ALM) to Basel III standards before the standardization deadline of 2028.

.jpg)

Furthermore, Yuanta Securities Vietnam believes that Circular 25 helps improve profit margins. Using low-cost short-term capital to finance higher-interest long-term loans will help banks improve their net interest margin (NIM).

A notable point in this easing is the facilitation of long-term capital flows. "Backbone" sectors such as highways, seaports, wind power, solar power, and industrial parks will have a more stable supply of capital.

At the same time, excluding outstanding loans for social housing from the real estate credit growth limit helps capital flow into segments with real demand

According to VCBS's calculations, increasing the maximum ratio of short-term capital used for medium and long-term lending to 40% could help the banking system add approximately 1 trillion VND in medium and long-term loans to the economy. Credit growth could reach 17% in 2026. This will be the "lifeblood" nurturing the green and digital economy, supporting the goal of sustainable growth

Despite its easing nature, the State Bank of Vietnam's message remains consistent: credit expansion must be focused. The new policies are not a general loosening but rather a flexible adjustment to direct funds into production and priority sectors.

For these monetary policies to be truly effective, coordination with fiscal policy – especially the speed of public investment disbursement – will be a crucial lever for genuinely and sustainably lowering interest rates